Simon Hughes looks at the latest trends in dental practice sales for NHS, mixed, and private practices, as well as the growth of corporate bodies.

Simon Hughes looks at the latest trends in dental practice sales for NHS, mixed, and private practices, as well as the growth of corporate bodies.

At Christie & Co, we value or sell well over 350 dental practices each year. This activity gives us an insight into the market to assess average sale prices on different practice types.

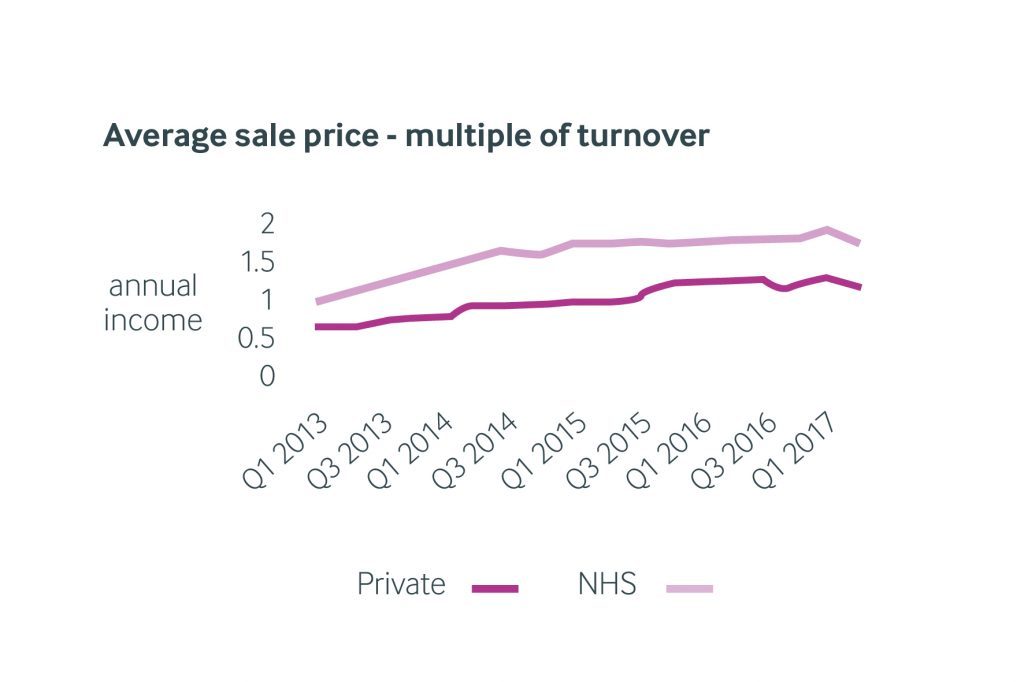

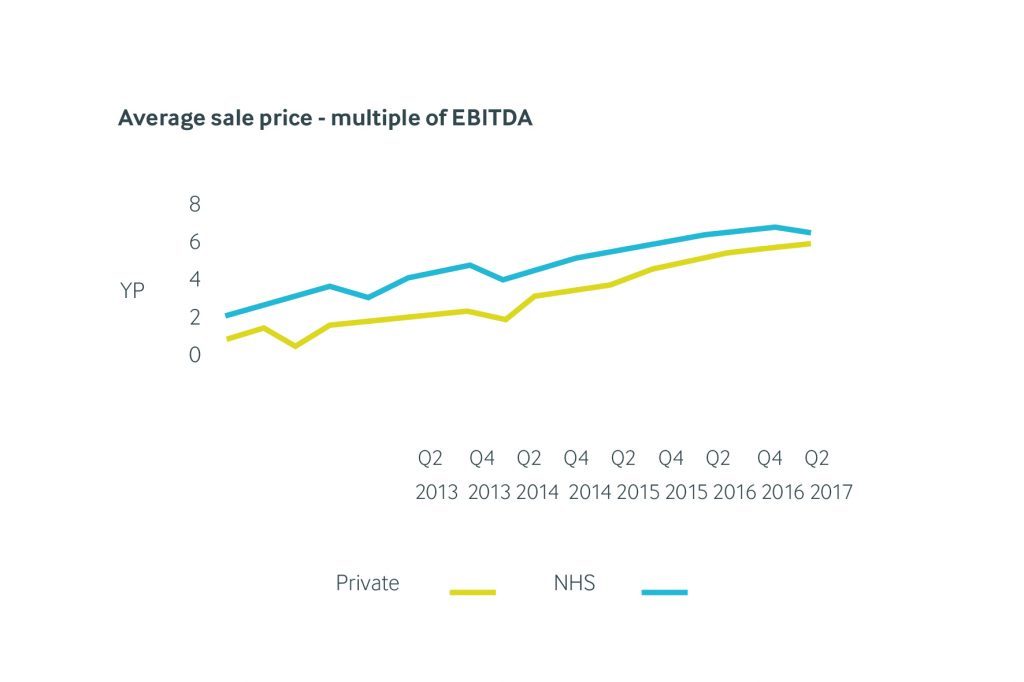

The graphs to the right illustrate the average movement in prices since the beginning of 2013, expressed as multiples of turnover and EBITDA (earnings before interest, tax, depreciation and amortisation).

It’s interesting to see that both types of practice – NHS, mixed and private – have shown steady increases in multiples, and more recently highlighting that private practice multiples are catching up with NHS/mixed practices, reflecting the resurgence of this segment of the market.

Historically, dental practices have been valued on a ‘pence in the pound’ approach, but as the market becomes more sophisticated this is being replaced by multiples of profit or EBITDA.

This is the number upon which banks base their decision to lend, as it points to the ability of the business to service debt.

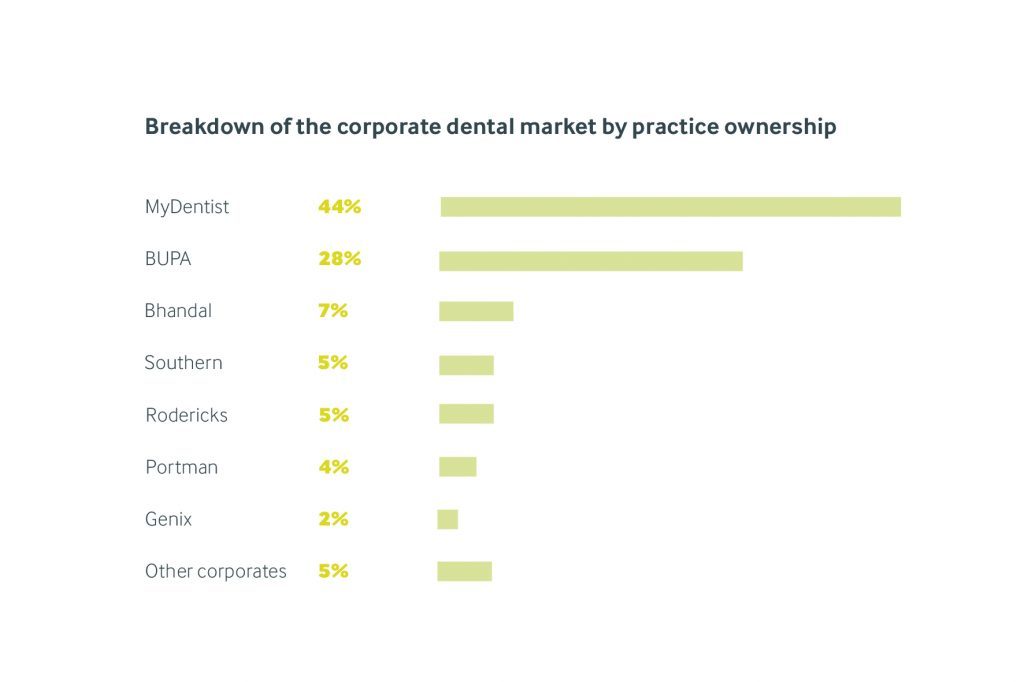

Compared to many others, the dental sector is highly fragmented with a relatively small percentage of practices owned by corporate owners.

This makes it highly attractive to expanding multiple practice owners and other types of buyers such as investors, who are able to rapidly acquire practices to consolidate the industry.

Until very recently, only Oasis (now owned by Bupa) and Mydentist have been significantly backed by private equity.

However, the recent acquisition of Southern Dental by Jacob’s Holding and of Genesis by August Equity, signal the entry into the dental sector of a new breed of purchaser.

For more information on Christie & Co, visit www.christie.com, email [email protected] or call 020 7227 0700.